Ready For EPF’s Account 3? Initial Amount Transfer Will Go Live 12 May

Get familiar with the new EPF accounts and the much-awaited flexible withdrawal feature.

Subscribe to our FREE Newsletter, or Telegram and WhatsApp channels for the latest stories and updates.

For as long as we have all been contributing to the Employees Provident Fund (EPF), withdrawing cash is not allowed.

This all changed when Covid-19 hit and the government allowed for several special withdrawals from Account 2 to help people with their finances during the pandemic.

The special withdrawals have since stopped and we have all gone back to the EPF we know, where cash withdrawals are not allowed until you hit 50.

In a historic move, the EPF recently announced the introduction of Account 3.

READ MORE: EPF Confirms Account 3 To Launch 11 May

Funds from Account 3 can be withdrawn at any time (subject to terms and condition).

So what is Account 3 exactly?

While Account 3 will go live on 11 May (Saturday), take note that the date of initial funds transfer to Account 3 will start from 12 May (Sunday).

This probably has something to do with EPF recently announcing that their online system will undergo disruption on 10 and 11 May.

READ MORE: EPF Announces Online System Disruption On Same Day As Account 3 Going Live

Here’s a simple breakdown of what this account restructuring is.

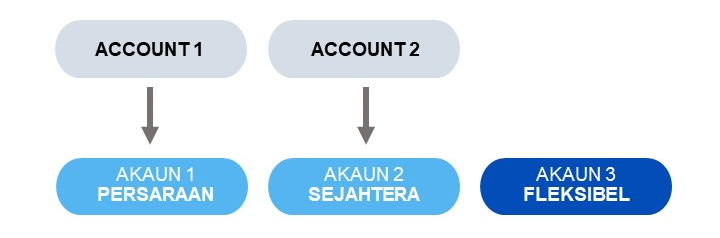

Renaming of EPF accounts

While we are all familiar with Account 1 and Account 2 when it comes to our EPF contribution, this will change come Saturday.

Account 1 – Akaun Persaraan

Account 2 – Akaun Sejahtera

Account 3 – Akaun Fleksibel

What is Akaun Persaraan?

Akaun Persaraan, originally Account 1, is renamed to suit the purpose or objective of the account. This account aims to accumulate and increase the members’ saving level for the long term in order to achieve comfortable life after retirement.

Savings in Akaun Persaraan cannot be withdrawn before the member reaches 55 years old. However, eligible members can invest a portion of their Akaun Persaraan savings in investments managed by the approved Fund Management Institutions (FMIs), subject to the terms and conditions.

What is Akaun Sejahtera?

Akaun Sejahtera, originally Account 2, is renamed to suit the purpose or objective of the account. This account aims to meet the pre-retirement life cycle needs for the medium term which contributes to retirement wellbeing.

Savings in Akaun Sejahtera can be withdrawn for pre-retirement purposes (subject to EPF terms and conditions) such as: Housing, Education, Health, Insurance Protection, Hajj, Age 50.

What is Akaun Fleksibel?

This account is designed to meet members’ short-term financial needs.

Savings in Akaun Fleksibel can be withdrawn by members any time, subject to terms and conditions. However, members are encouraged to withdraw only for emergency purposes and immediate needs only.

Now that we’ve got the accounts sorted, let’s get into what this means, considering you can start to restructure your funds once this goes live.

What is EPF account restructuring?

The EPF account restructuring aims to enhance members’ income security after retirement while addressing their life cycle needs.

The account will be restructured from two accounts to three accounts as mentioned above.

Savings in Akaun Fleksibel can be accessed or withdrawn by members, subject to terms and conditions.

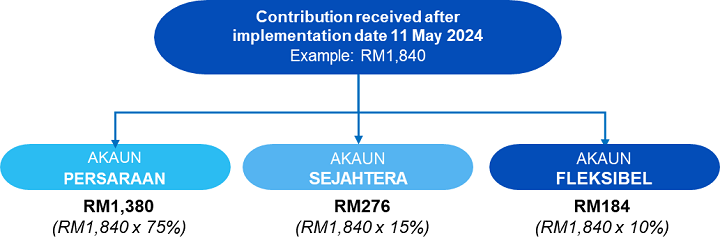

After the effective date, new EPF contributions will be credited according to the ratio of 75:15:10.

Is the EPF account restructuring applicable for all EPF members?

The restructuring of EPF accounts is applicable for all EPF members, including non-Malaysians who have yet to attain the age of 55 on 11 May 2024.

What will happen to the existing savings in Account 1 and Account 2 when the account restructuring is implemented?

Savings balances in Account 1 and Account 2 will remain in Akaun Persaraan and Akaun Sejahtera respectively, while Akaun Fleksibel will start with a zero balance.

How will the new contributions be credited after the implementation date of the account restructuring?

After the implementation date, new contributions will be distributed as follows:

The distribution of contributions are as illustrated below:

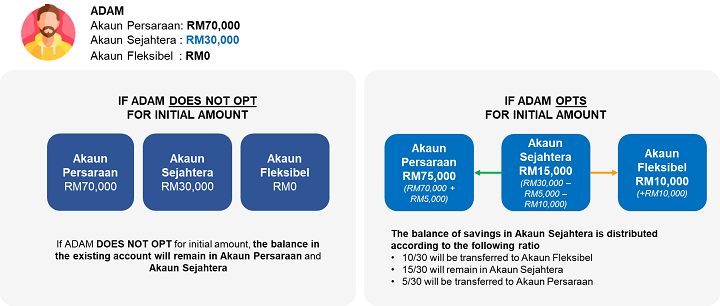

What is meant by the option for initial amount transfer?

After the implementation date, members have the option to transfer part of the savings balance (refer to question 12) in Akaun Sejahtera as an initial amount to Akaun Fleksibel.

How is the initial amount in Akaun Fleksibel determined?

The determination of the initial amount in Akaun Fleksibel is subject to the savings balance in members’ Akaun Sejahtera on the application date as follows:

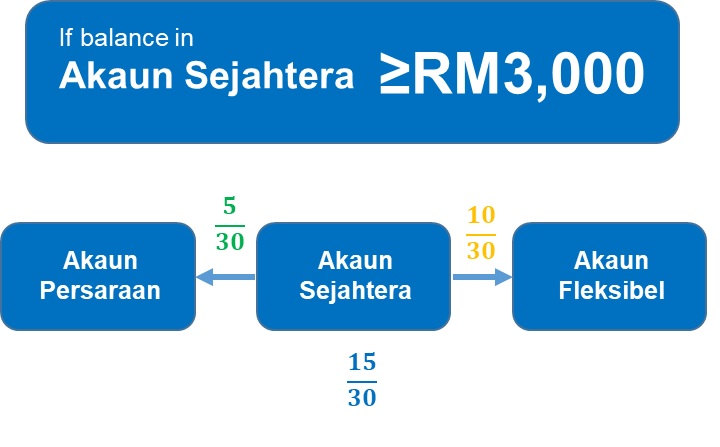

For members who have a savings balance of RM3,000 and above in Akaun Sejahtera

The balance of savings in Akaun Sejahtera is distributed according to the following ratio:

i. Ten out of thirty (10/30) of the Akaun Sejahtera savings will be transferred to the Akaun Fleksibel.

ii. Five out of thirty (5/30) of the Akaun Sejahtera will be transferred to the Akaun Persaraan.

iii. The balance of fifteen out of thirty (15/30) will remain in the Akaun Sejahtera.

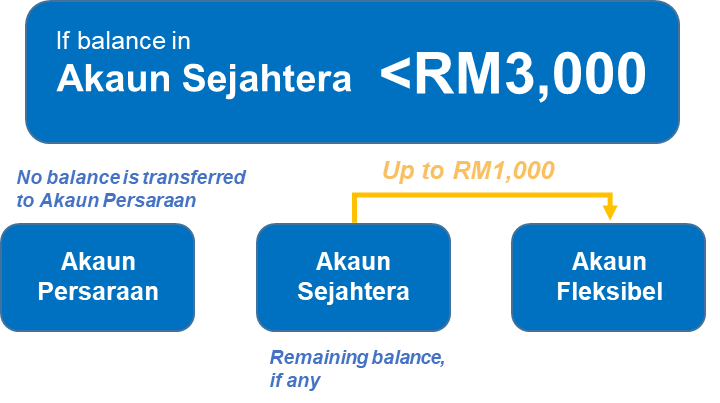

Transfer of savings balance of less than RM3,000 in Akaun Sejahtera will be made as follows:

i. Akaun Sejahtera with savings of RM1,000 and below, the entire amount will be transferred to the Akaun Fleksibel.

ii. Akaun Sejahtera with savings of more than RM1,000 and not exceeding RM3,000, the amount transferred to the Akaun Fleksibel is RM1,000, while the balance will remain in the Akaun Sejahtera.

iii. No distribution will be made to the Akaun Persaraan for those whose savings in Akaun Sejahtera is less than RM3,000.

How can a member apply for the initial amount transfer?

KWSP i-Akaun or Self-Service Terminal (SST) at any EPF office.

When can a member make the option for initial amount transfer?

Members can opt for the initial amount transfer starting from 12 May 2024 until 31 August 2024. This application can only be made once at any time during the period and cannot be cancelled.

What happens if the member did not opt for the initial amount transfer?

If a member chooses not to have an initial amount transfer to Akaun Fleksibel, the balance in the existing account will remain in Akaun Persaraan and Akaun Sejahtera.

Meanwhile, new contributions starting 11 May 2024 will be credited into Akaun Persaraan, Akaun Sejahtera, and Akaun Fleksibel.

When will the initial amount transfer to Akaun Fleksibel be approved?

The initial amount transfer will be approved within 3-5 working days.

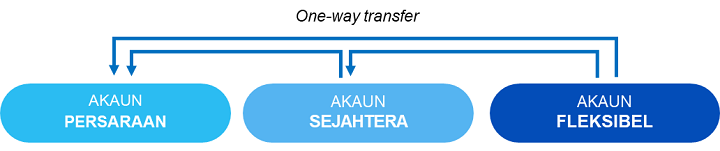

Can a member transfer their savings from Akaun Fleksibel to Akaun Sejahtera or Akaun Persaraan?

Members can transfer their savings as follows:

Akaun Fleksibel to Akaun Sejahtera

Akaun Fleksibel to Akaun Persaraan

Akaun Sejahtera to Akaun Persaraan

Savings can only be transferred in one direction and cannot be reversed back into the original account. There is no limit on the amount that can be transferred between accounts.

Can members apply to transfer their savings?

At this moment, members may submit a savings transfer application at any EPF Offices by completing the “Savings Transfer To Akaun Persaraan/ Akaun Sejahtera Form (KWSP 12)”.

Let’s Talk Withdrawal

So when can we withdraw from Akaun Fleksibel? Members can apply for Akaun Fleksibel Withdrawal as soon as Akaun Fleksibel has a minimum balance of RM50 either after the transfer of the initial amount from Akaun Sejahtera has been made or after the crediting of new contributions.

What are the conditions for Akaun Fleksibel withdrawal?

Below 55 years old.

Have savings in Akaun Fleksibel.

Minimum withdrawal limit is RM50.

How to withdraw?

Either through your KWSP i-akaun app or website, or EPF offices.

Do members need to submit any supporting documents when applying?

Members do not need to submit any supporting documents. However, an active bank account number need to be submitted to ensure a smooth payment processing.

Thumbprint verification in person?

Generally, members do not need to be physically present for identity verification at EPF Offices as it can be done online; however, it is subject to the member’s previous withdrawal history and the withdrawal amount does not exceed RM30,000.

For members who do not have previous withdrawal history, or their bank account information differs from previous withdrawal records, members need to perform identity verification through:

- Thumbprint verification via Self-Service Terminal (SST) at any EPF Offices, for withdrawal application amount of more than RM10,000; OR

- Online verification, subject to withdrawal application amount of less than RM10,000.

What is the payment method for Akaun Fleksibel withdrawal?

Akaun Fleksibel Withdrawal payments will be direct credited into the member’s bank account. To ensure ease of receiving Akaun Fleksibel Withdrawal payments, please ensure the following conditions are met:

Bank account (savings or current account) status is active; and bank account is registered under the member’s own name (not a joint/ company account).

REMINDER: Members who do not have a bank account are advised to open a bank account before applying for Akaun Fleksibel Withdrawal.

When will you get your money?

Payment will be made within seven working days upon application approval.

Is there a difference in dividend rate?

At this time, the restructuring of EPF account will not change the current policy on establishing dividend rates. The same dividend rate will apply to all three accounts.

For more information, check out the EPF FAQ.

Share your thoughts with us via TRP’s Facebook, Twitter, Instagram, or Threads.